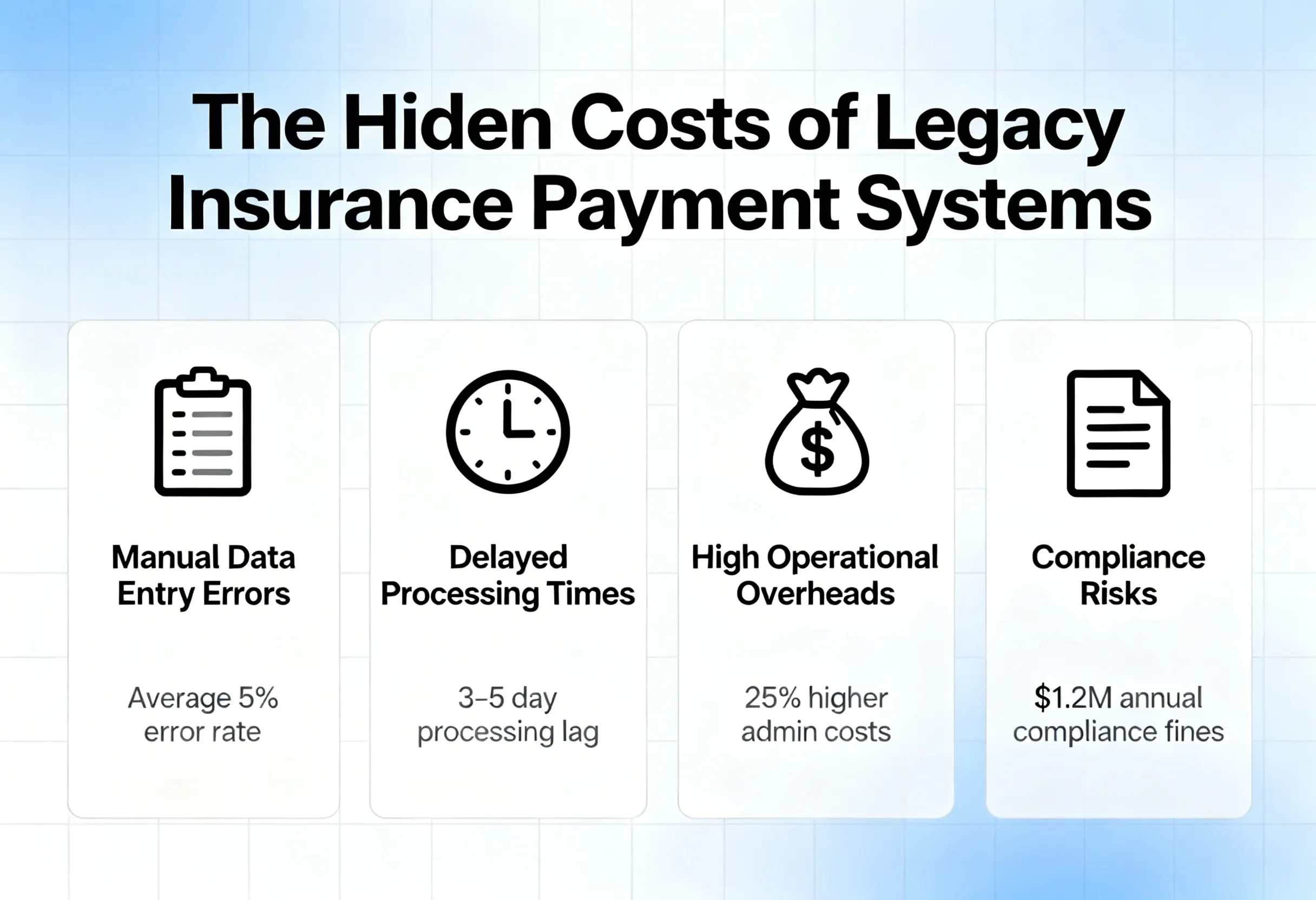

Many insurance companies still rely on outdated payment infrastructure built decades ago. While these systems may appear stable, they quietly drain millions through inefficiencies, fraud exposure, reconciliation errors, compliance risks, and customer churn.

In 2026, insurance payments are expected to be real-time, automated, and customer-centric. Legacy systems struggle to keep up. This blog explores the hidden costs of outdated insurance payment systems, the operational and financial impact, and how modern payment platforms can transform profitability.

Why Legacy Insurance Payment Systems Are Costing Millions

Insurance leaders often focus on underwriting performance and claims ratios. However, payment infrastructure is an overlooked cost center that directly affects revenue, retention, and operational efficiency.

Legacy payment systems are not just old. They are expensive to maintain and even more expensive to ignore.

1. High Operational and Maintenance Costs

Older payment systems require constant manual intervention, patchwork integrations, and specialized IT support. Many insurers maintain multiple disconnected systems for premium collection, claims disbursement, and agent payouts.

Where the Costs Add Up

| Cost Area | Impact on Insurers |

| Manual reconciliation | Increased labor expenses |

| System maintenance | High IT resource allocation |

| Multiple vendors | Overlapping licensing costs |

| Limited automation | Slower processing cycles |

These inefficiencies compound over time, significantly inflating operational budgets.

2. Revenue Leakage and Failed Transactions

Outdated systems often lack intelligent retry mechanisms, smart routing, and real-time validation. This leads to failed payments, delayed settlements, and gaps in premium collection.

Common Revenue Leak Points

| Issue | Financial Impact |

| Payment failures | Missed premium collections |

| Delayed claim payouts | Increased customer dissatisfaction |

| Chargebacks | Higher dispute costs |

| Manual errors | Incorrect posting of payments |

Even a small percentage of failed transactions can translate into millions in lost or delayed revenue for mid-sized insurers.

3. Poor Customer Experience

Today’s policyholders expect seamless digital experiences similar to e-commerce platforms. Legacy payment systems often offer limited payment options, slow confirmations, and rigid billing structures.

Customer Friction Points

- Limited digital wallet support.

- No instant confirmation.

- Inflexible installment options.

- Slow refund processing.

When payment experiences feel outdated, customers associate that frustration with the insurer.

4. Compliance and Security Risks

Insurance payments involve sensitive financial data. Legacy systems often lack advanced security features like tokenization, end-to-end encryption, and automated compliance updates.

Risk Comparison

| Legacy Systems | Modern Platforms |

| Periodic security updates | Continuous security monitoring |

| Manual compliance checks | Automated compliance workflows |

| Higher fraud exposure | AI-driven fraud detection |

| Limited reporting | Real-time audit trails |

Data breaches, compliance penalties, and fraud incidents can cost insurers millions in direct losses and reputational damage.

5. Slow Reconciliation and Financial Reporting

Finance teams often spend days reconciling payments across multiple systems. Manual reporting delays month-end closing and reduces visibility into real-time cash flow.

Impact on Finance Teams

- Longer closing cycles.

- Increased accounting errors.

- Limited transaction transparency.

- Poor forecasting accuracy.

Modern unified platforms automate reconciliation and provide real-time dashboards.

6. Inability to Scale with Growth

As insurers expand into new states, products, or digital channels, legacy payment systems struggle to scale. Adding new payment methods or integrations often requires significant redevelopment.

Scaling Challenges

| Growth Initiative | Legacy System Limitation |

| New digital channels | Complex integrations |

| Embedded insurance partnerships | Limited API capabilities |

| Real-time payments | Infrastructure constraints |

| Subscription billing models | Rigid architecture |

Modern payment platforms like Tranzpay are built with flexible APIs, automation tools, and scalable infrastructure to support future growth.

Conclusion

Legacy insurance payment systems are costing millions through operational inefficiencies, revenue leakage, security risks, and customer churn. While these systems may appear functional, their hidden costs accumulate across departments.

In 2026, payment infrastructure must be real-time, automated, secure, and scalable. Insurers that modernize their payment ecosystems will reduce costs, improve customer satisfaction, and unlock new revenue opportunities.

Modernization is no longer optional. It is a financial necessity.

Frequently Asked Questions

- What is a legacy insurance payment system?

A legacy insurance payment system is an outdated payment infrastructure that relies on manual processes, limited automation, and older technology frameworks. - How do legacy payment systems cost insurers money?

They increase operational costs, cause revenue leakage, create compliance risks, and reduce customer retention due to poor payment experiences. - What are the biggest risks of outdated payment systems?

The biggest risks include fraud exposure, data breaches, reconciliation errors, failed transactions, and the inability to scale. - How can insurers reduce payment-related losses?

Insurers can adopt modern payment platforms that offer automation, real-time processing, intelligent routing, and advanced fraud detection. - Why is payment modernization important in 2026?

Customer expectations, regulatory requirements, and digital transformation trends demand faster, more secure, and scalable payment infrastructure.