The 2026 Nacha risk management rules expand fraud-monitoring expectations across ACH participants and require businesses to implement risk-based controls designed to detect unauthorized or deceptive payments, including those approved under false pretenses.

Why This Matters Now

Finance and operations teams are being asked to do two things at once:

- Move money faster

- Make the process less fragile

That tension is increasing, not decreasing. ACH volume continues to grow, Same Day ACH is expanding, and fraud tied to payment instructions is becoming more sophisticated.

When a business is tricked into sending funds to the wrong account, the payment may still appear authorized.

The failure often happens before the payment is created.

What Changed in 2026

Core shift

The 2026 rules move ACH risk from after-the-fact detection → proactive workflow control

What actually changed

- Risk-based fraud monitoring is now expected

- “Authorized under false pretenses” is explicitly included

- Standardized payment descriptors introduced

- Broader participant coverage in Phase 2

What this means in practice

Compliance is no longer just about:

- file formatting

- approvals

- return rates

It now includes:

- suspicious activity detection

- account-change validation

- payout visibility

- structured escalation paths

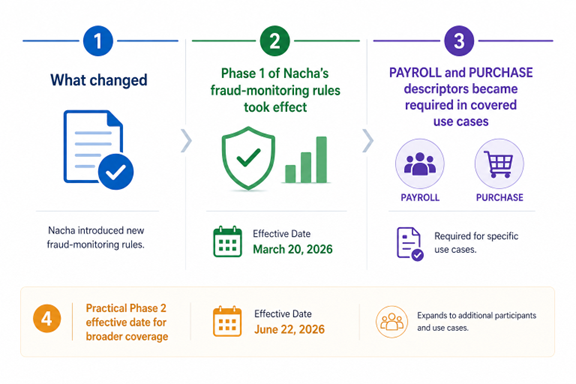

Key Timeline at a Glance

| Date | What Changed | Why It Matters |

| March 20, 2026 | Phase 1 fraud-monitoring rules took effect | Shift from awareness → documented risk-based processes |

| March 20, 2026 | PAYROLL and PURCHASE descriptors required | Improves monitoring, exception handling, fraud response |

| June 22, 2026 | Phase 2 expands coverage | More businesses and institutions come into scope |

What “Authorized Under False Pretenses” Actually Means

This is the most important concept in the 2026 rules.

It refers to payments that:

- were technically approved

- but approved based on fraudulent instructions

Common examples

- Vendor banking changes via email

- Payroll account updates

- Executive impersonation requests

- Urgent payout instructions

- First-time payment destinations

By the time the payment reaches ACH, it looks valid.

The risk exists inside your workflow

Who Is Affected

The rules apply across ACH participants, including:

- ODFIs

- Non-consumer Originators (business senders)

- Third-Party Senders

- Third-Party Service Providers

- RDFIs above threshold levels

Phase 2 (June 2026) expands this further.

What Businesses Are Actually Expected to Do

Nacha does not prescribe tools. It expects risk-based processes.

In practice, that means:

- Treat first-time payments differently from recurring ones

- Verify bank account changes through a second channel

- Apply controls based on risk, not just dollar amount

- Monitor patterns, timing, and anomalies

- Define clear escalation workflows

Payment Descriptors: Why They Matter

As of March 2026:

- PAYROLL → required for certain compensation payments

- PURCHASE → required for certain WEB debit use cases

This is not just formatting.

It improves:

- transaction clarity

- anomaly detection

- fraud response

Businesses that ignore payment data quality will fall behind.

Biggest Operational Risks for Businesses

Fraud does not enter at the bank level first.[Text Wrapping Break] It enters inside workflows

Key risk areas

- Vendor bank account changes

- Executive impersonation scams

- First-time payment destinations

- Low-visibility outbound payments

- Manual workflows outside approval systems

Practical Preparation Plan for Finance Teams

This is where most companies overcomplicate things.[Text Wrapping Break] The fix is usually operational, not technical.

What to do now

- Tighten bank-detail change controls

- Add second-channel verification

- Use account validation where needed

- Review approvals by risk level

- Improve visibility into payment activity

- Define response steps for suspect payments

Operational Checklist

- Review all ACH workflows (payroll, vendors, refunds, claims)

- Map where instructions enter your system

- Identify where fraud can occur

- Assign responsibility (internal, bank, provider)

- Monitor unusual activity patterns

- Define escalation and response ownership

Where Tranzpay Fits

This is not just a compliance problem. It is a workflow problem.

Tranzpay aligns with the operational side of these changes by supporting:

- payment verification

- bank processing

- reporting and visibility

- customer vaulting

- outbound payment workflows

The goal is not more manual checks

The goal is better visibility + controlled workflows

Bottom Line

The 2026 Nacha rules are not just a rule update.

They are a shift in how ACH risk is managed.

Businesses that treat this as:

- a checklist → will struggle

- an operating model upgrade → will benefit

ACH remains one of the most efficient payment rails.

But it now requires workflow-level controls, not just bank-level validation.

FAQs

- What are the 2026 Nacha risk rules?

They expand fraud-monitoring expectations and require risk-based procedures to identify suspicious or deceptive ACH entries. - Do these rules apply to businesses sending ACH?

Yes. Businesses acting as non-consumer Originators are included in the framework. - What does “authorized under false pretenses” mean?

A payment approved based on deception, such as fraudulent account changes or impersonation. - Do businesses need to review every payment manually?

No. The rules support a risk-based approach, not universal manual review. - What should teams do before June 22, 2026?

Review workflows, tighten controls, improve visibility, and define escalation processes.