For insurance finance teams, ACH payments are no longer just a back-office function. They sit at the center of premium collections, claim payments, refunds, commissions, vendor payments, and day-to-day cash movement.

That also makes ACH errors more expensive.

A mistyped account number can delay a claim payment. A bad routing number can create return fees and manual follow-up. A fraudulent account change can send funds to the wrong destination. For insurers managing high transaction volumes across policyholders, producers, vendors, and claimants, even a small error rate can create a long trail of rework.

In 2026, account validation has become a practical control for reducing that risk. Nacha describes account validation as a best practice for organizations sending payments and notes that validating first-use consumer account information is addressed through its Account Validation Rule.

For insurance carriers, MGAs, TPAs, brokers, and finance teams, the goal is simple: confirm that bank account information is usable before money moves.

What Is Account Validation?

Account validation is the process of checking bank account details before initiating an ACH debit or credit.

At a basic level, it helps confirm whether the routing number and account number are formatted correctly and whether the account appears valid. More advanced account validation can also help assess whether the account is open, active, eligible for ACH, and associated with the expected account holder.

For insurance finance teams, this matters in both payment directions:

- Incoming payments: Premiums, deductibles, policy fees, installment payments, and receivables.

- Outgoing payments: Claims, premium refunds, producer commissions, vendor payments, legal settlements, and other disbursements.

Insurance payments move in both directions, and missed premium payments or delayed claim payments can affect both operations and customer experience.

Why Account Validation Matters More in 2026

ACH has always required accuracy, but the risk environment is changing. Finance teams are dealing with faster payment expectations, more digital enrollment, higher fraud attempts, and tighter ACH risk requirements.

Nacha’s 2026 fraud monitoring rule changes are part of a broader risk management package intended to reduce successful fraud attempts and improve recovery after fraud occurs. Phase 2 fraud monitoring amendments become effective June 19, 2026, with the practical effective date falling on Monday, June 22, 2026, because June 19 is a federal holiday.

For insurance organizations, these changes matter because ACH activity touches several sensitive workflows: claim payouts, premium drafts, refunds, producer commissions, payroll, and vendor payments.

The message for finance leaders is clear: account validation should not be treated as a one-time technical check. It should be part of a broader payment risk process.

The Cost of ACH Errors in Insurance Finance

ACH errors are rarely isolated. One failed transaction can create work across finance, customer service, claims, billing, and compliance.

Common causes include:

- Incorrect routing numbers

- Closed or invalid accounts

- Mistyped account numbers

- Account ownership mismatches

- Fraudulent account changes

- Duplicate account entries

- Outdated payment instructions

- Policyholder or claimant data entered through manual forms

When an ACH transaction fails, the finance team often has to identify the return reason, contact the customer or payee, collect corrected information, update internal systems, retry the payment, reconcile the exception, and document the issue.

That work adds up quickly.

For an insurer, the problem is not only the return fee. It is the operational drag around every failed payment. A failed premium draft may put a policy at risk of lapse. A failed claim payment may increase call volume. A failed commission payment may frustrate producers. A failed refund may create avoidable complaints.

Account validation reduces these problems by catching bad information earlier in the process.

ACH Returns: The Metric Finance Teams Cannot Ignore

ACH returns are one of the clearest signs that payment data quality needs attention.

Nacha has established return rate thresholds that organizations monitor closely. Unauthorized debit returns have a threshold of 0.5%, administrative returns have a threshold of 3.0%, and the overall return rate threshold is 15.0%. Administrative returns commonly include issues such as incorrect account information or routing numbers.

For insurance finance teams, administrative returns are especially important because they are often preventable. They usually point to data entry issues, outdated account records, onboarding gaps, or weak validation at the point of enrollment.

A mature payment operation should track:

- Return rate by payment type

- Return rate by business unit

- Return reason codes

- First-time payment failure rates

- Repeat failures by customer or vendor

- Manual hours spent on payment exceptions

- Reissued payment volume

- Claims or refund delays caused by failed ACH

These numbers help finance leaders move the discussion from “payment errors happen” to “we know where errors happen, why they happen, and how to reduce them.”

Where Insurance Teams Should Use Account Validation

Account validation is most useful at the points where bank account information is first collected, changed, or reused after a long gap.

1. Premium Payment Enrollment

When a policyholder enrolls in ACH for recurring premium payments, the account should be validated before the first debit. This reduces failed drafts, billing exceptions, and customer service follow-up.

It also helps prevent situations where incorrect payment details create downstream coverage issues.

2. Claims Disbursements

Claim payments are time-sensitive. A failed ACH payment can delay funds when the policyholder or claimant is already dealing with a stressful event.

For claim payouts, account validation helps confirm that payment instructions are usable before funds are released. It is especially important for first-time claimants, high-value payments, catastrophe-related payouts, and account changes requested late in the claim process.

3. Premium Refunds

Refunds often involve customers who may not be actively engaged with the insurer anymore. If the account on file is outdated, the refund may fail and require manual outreach.

Validating the account before issuing the refund can reduce rework and improve refund completion rates

4. Producer and Agent Commissions

Producer payments often involve recurring ACH credits. The risk increases when banking details are changed, agencies consolidate, or commission payments are redirected.

Finance teams should validate new or changed payment instructions before the next commission run.

5. Vendor and Service Provider Payments

Insurers work with repair networks, legal firms, medical providers, adjusters, inspection companies, and other partners. A fraudulent vendor banking update can create serious loss exposure.

Account validation should be paired with approval controls for vendor banking changes.

Account Validation and Fraud Prevention

Account validation is not the same as full fraud prevention, but it is a core layer in the payment control process.

Fraud often enters through account changes, impersonation, compromised emails, fake vendors, synthetic identities, or manipulated payment instructions. Federal banking agencies have continued to focus on payment fraud risk, including scams and illegal attempts to make or receive payments for personal gain.

For insurers, common risk scenarios include:

- A fraudster changes claimant banking details

- A producer commission account is redirected

- A vendor impersonator submits new ACH instructions

- A policyholder uses invalid or stolen account information

- A refund is routed to an account that does not belong to the expected recipient

- A payment file contains account changes that were not properly reviewed

Account validation helps finance teams catch some of these issues before payment release. Stronger programs combine validation with identity checks, approval workflows, change monitoring, exception reporting, and audit trails.

The key is to validate at the right moments, not only during initial onboarding.

What Finance Teams Should Validate Before an ACH Payment

A practical account validation process should check more than whether the account number has the right number of digits.

Depending on the payment type and risk level, finance teams should consider validating:

- Routing number status: Is the routing number valid and associated with a financial institution that can receive ACH entries?

- Account format: Does the account number follow expected formatting rules?

- Account status: Does the account appear open and active?

- ACH eligibility: Can the account receive the type of ACH transaction being initiated?

- Account ownership alignment: Does the account appear connected to the expected policyholder, claimant, producer, vendor, or business entity?

- Change history: Was the account recently changed, and does that change need additional review?

- Risk signals: Is the payment amount, timing, location, or account change unusual compared with normal activity?

Not every payment needs the same level of review. A $25 recurring premium draft and a six-figure claim settlement do not carry the same risk. A good process applies stronger checks when the risk is higher.

How Account Validation Reduces Manual Rework

Finance teams often feel payment problems after the damage is already done. The payment fails, the return code arrives, the customer calls, the claim team escalates, or the reconciliation queue grows.

Account validation moves the work earlier.

Instead of repairing failed payments after submission, teams can prevent many failures before payment initiation.

That means fewer:

- ACH returns

- Reissued payments

- Manual bank detail corrections

- Calls to policyholders or claimants

- Payment status escalations

- Reconciliation exceptions

- Claim payment delays

- Duplicate payment risks

- Internal emails between finance, billing, claims, and service teams

The operational benefit is especially strong for insurers because payments are spread across multiple systems. Billing, policy administration, claims, producer management, and accounting systems may all contain payment data. When bad account information enters one system, the error can travel.

Account validation gives finance teams a control point before that error turns into a failed payment.

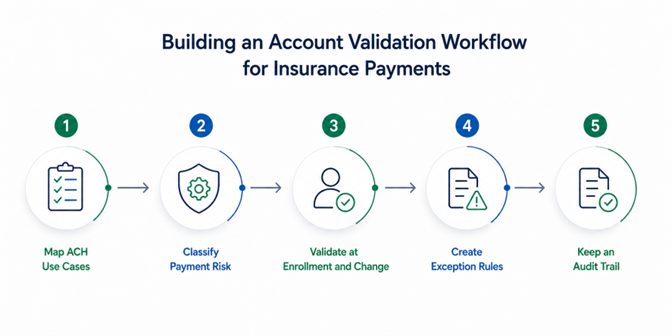

Building an Account Validation Workflow for Insurance Payments

A strong account validation workflow does not have to be complicated. It should be consistent, documented, and built around the points where payment risk is highest.

Step 1: Map ACH Use Cases

Start by listing every ACH workflow across the organization.

Include:

- Premium drafts

- Claim payments

- Refunds

- Commission payments

- Vendor payments

- Payroll

- Third-party administrator payments

- Legal or settlement payments

Then identify where account information is collected, stored, changed, approved, and sent for payment.

Step 2: Classify Payment Risk

Not every ACH transaction needs the same controls.

Classify payments by:

- Dollar amount

- Payment direction

- First-time account use

- Account changes

- Recipient type

- Urgency

- Business unit

- Fraud exposure

- Regulatory or audit sensitivity

This helps finance teams apply the right level of validation without slowing every payment.

Step 3: Validate at Enrollment and Change

At minimum, validate accounts when:

- A new policyholder enrolls in ACH

- A claimant adds direct deposit details

- A vendor submits banking instructions

- A producer changes commission payment details

- A refund is going to an account not previously used

- A dormant account is reused

- A high-value payment is scheduled

- The highest-risk moment is often not the first payment. It is the account change.

Step 4: Create Exception Rules

Validation should not simply return a pass or fail. Finance teams need clear exception rules.

For example:

- If the account is invalid, block the payment and request corrected details

- If the account ownership does not match, route for review

- If banking details changed within a defined period before payment, require secondary approval

- If the payment amount exceeds a threshold, require additional verification

- If the return history is poor, restrict automatic retries

These rules help teams avoid inconsistent manual decisions.

Step 5: Keep an Audit Trail

Account validation should leave a record.

Finance, compliance, and internal audit teams should be able to see:

- When validation occurred

- Which account was validated

- What result was returned

- Who approved any exception

- What action was taken

- Whether the payment was released, held, corrected, or canceled

This is especially important as ACH risk management expectations continue to increase.

Account Validation for Claims Payments: A Practical Example

Consider a property insurer issuing claim payments after a severe weather event.

Without account validation, the team may collect claimant bank details through a portal, push the payment file, and find out later that some payments failed because of incorrect account numbers, closed accounts, or mismatched recipient details.

That creates several problems:

- Claimants call to ask where the payment is

- Adjusters spend time checking payment status

- Finance has to research returns

- Payments need to be reissued

- Reconciliation is delayed

- Customer satisfaction drops during a high-stress claim event

With account validation, the insurer can check account details before release, flag exceptions, and correct issues before the payment file is sent.

This does not remove every risk. But it reduces avoidable failures and gives the finance team better control over high-volume disbursement periods.

Account Validation for Premium Payments: A Practical Example

Now consider recurring premium payments.

A policyholder enters bank details for monthly ACH drafts. If the account number is mistyped, the first debit may fail. That can trigger billing notices, service calls, late payment handling, retry logic, and possible policy disruption.

With account validation at enrollment, the insurer can catch the issue before the first draft.

For finance teams, this helps reduce administrative returns. For billing teams, it reduces follow-up. For policyholders, it creates a cleaner payment experience.

The benefit is not dramatic in one transaction. It becomes significant across thousands or millions of recurring payments.

What to Look for in an Account Validation Approach

Insurance finance teams should look for an approach that fits their payment volume, systems, and risk profile.

Key capabilities to evaluate include:

- Real-time validation: Useful when account details are entered through portals, payment forms, call centers, or service workflows.

- Batch validation: Useful for payment files, commission runs, refund files, and account clean-up projects.

- Support for inbound and outbound payments: Insurance teams need controls for premium collection and disbursements.

- Account ownership checks: Helpful for detecting mismatches between the expected recipient and the bank account.

- Change monitoring: Important for vendor updates, producer commission changes, and claimant payment changes.

- Exception reporting: Finance teams need clear queues for invalid, risky, or mismatched accounts.

- Audit-ready records: Validation history should support internal controls, compliance review, and payment investigations.

- Integration with existing systems: The process should fit billing, claims, accounting, ERP, treasury, and payment workflows without forcing teams into duplicate data entry.

Why Insurance Finance Teams Should Act Now

Account validation is not only a compliance topic. It is a finance operations topic.

For insurers, stronger validation can help reduce:

- ACH returns

- Fraud exposure

- Claim payment delays

- Premium collection failures

- Manual payment corrections

- Reconciliation issues

- Customer and producer escalations

- Internal audit gaps

The business case is strongest when finance teams measure both direct and indirect costs. Direct costs include return fees and reissued payments. Indirect costs include staff time, delayed reconciliation, customer service volume, claims escalations, and fraud investigation work.

In 2026, finance leaders should treat account validation as part of payment quality control.

How Tranzpay Helps Insurance Finance Teams Strengthen Payment Controls

Insurance payments are complex because money moves across many parties: policyholders, claimants, producers, vendors, TPAs, and internal business units.

Tranzpay helps finance teams manage inbound and outbound payment workflows with the controls needed to reduce payment friction, improve visibility, and support cleaner reconciliation.

For insurers, account validation can play an important role in that process by helping teams verify bank account details before ACH payments are initiated. When paired with practical approval rules and exception handling, it gives finance teams a better way to reduce errors, prevent avoidable rework, and lower payment risk.

The outcome is not just fewer failed transactions. It is a more reliable payment operation.

Final Takeaway

Account validation is one of the most practical steps insurance finance teams can take to improve ACH payment quality in 2026.

It helps reduce bad account data, prevent avoidable ACH returns, catch risky payment changes, and lower the manual work that follows failed payments. For insurers managing premiums, claims, refunds, commissions, and vendor payments, that control can make a measurable difference.

Finance teams do not need more payment complexity. They need cleaner account data, stronger controls, and fewer exceptions after the payment file is already out the door.

That is where account validation earns its place.

FAQs

- What is account validation in ACH payments?

Account validation is the process of checking bank account details before sending or collecting an ACH payment. It can help confirm whether the routing number and account number are valid, whether the account is open and eligible for ACH, and whether the account appears connected to the expected recipient. - Why is account validation important for insurance companies?

Insurance companies use ACH for premium collections, claim payments, refunds, commissions, and vendor payments. Account validation helps reduce failed payments, ACH returns, fraud risk, manual corrections, and payment delays. - How does account validation reduce ACH errors?

Account validation catches incorrect routing numbers, invalid account numbers, closed accounts, and other account issues before the payment is submitted. This helps finance teams prevent errors instead of fixing them after a return. - Can account validation help prevent ACH fraud?

Yes. Account validation can help reduce fraud risk, especially when paired with account ownership checks, change approvals, payment monitoring, and exception workflows. It is not a complete fraud prevention program by itself, but it is an important control. - When should insurance finance teams validate bank accounts?

Finance teams should validate bank accounts when a new ACH account is added, when payment details are changed, before first-time payments, before high-value disbursements, and when dormant accounts are reused. - What ACH workflows should insurers prioritize?

Insurers should prioritize claims payments, premium drafts, premium refunds, producer commissions, vendor payments, and any workflow where bank details are added or changed manually. - What are ACH administrative returns?

Administrative returns are ACH returns often tied to account data issues, such as incorrect account numbers or routing numbers. These are important for finance teams to track because many of them can be reduced through better validation. - Is account validation required by Nacha?

Nacha’s Account Validation Rule addresses validating first-use consumer account information for ACH payments, and Nacha describes account validation as a best practice for organizations sending payments. Organizations should work with their bank, processor, or compliance advisor to understand how the rules apply to their payment flows.